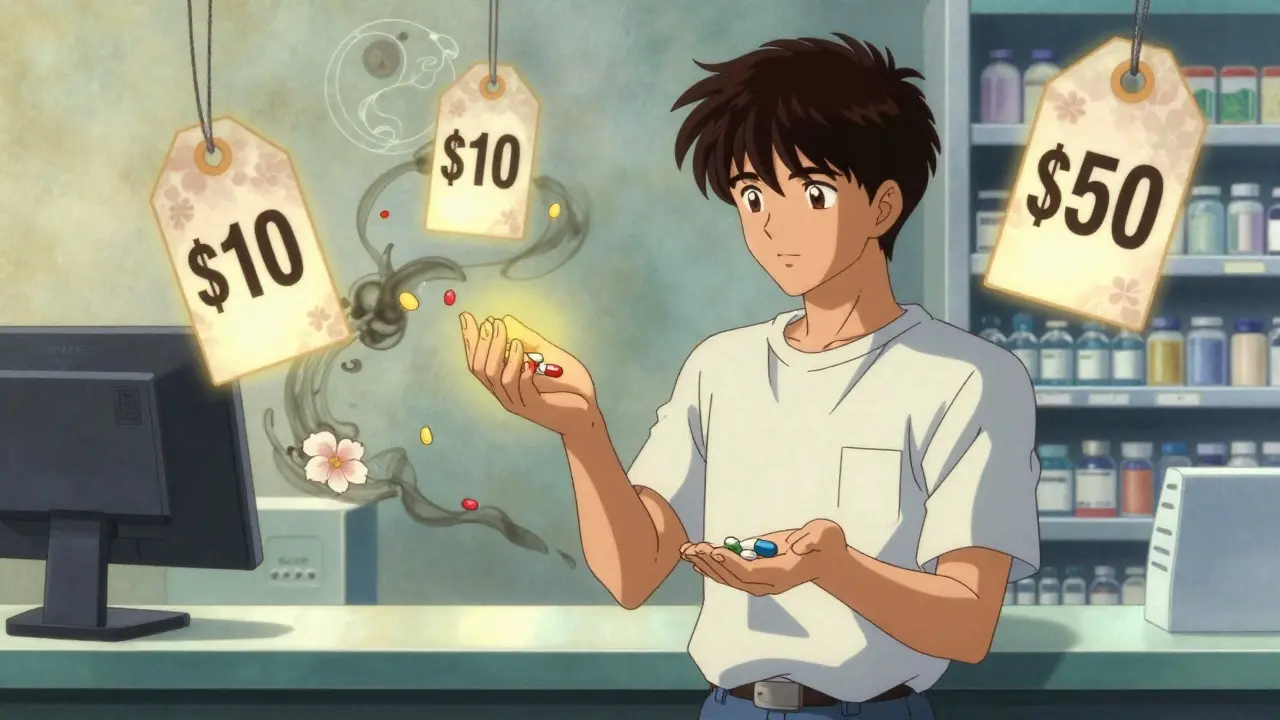

When you’re on multiple medications for conditions like high blood pressure, diabetes, or cholesterol, you might notice something strange: your insurance covers two separate generic pills for $10 each, but the generic combination pill that contains the same two ingredients costs $50. Why? It’s not a mistake. It’s how insurance formularies work-and understanding this can save you hundreds a year.

What Exactly Is a Generic Combination Drug?

A generic combination drug is a single pill that contains two or more active ingredients, all of which are already available as individual generics. For example, a common blood pressure combo pill might include lisinopril and hydrochlorothiazide-both available separately as generics. When the combination is approved by the FDA and goes generic, it becomes a single tablet that does the same job as taking two pills.

The FDA confirms that generic combination drugs are bioequivalent to their brand-name versions. That means they work the same way, have the same strength, and meet the same safety standards. So why isn’t the combo always cheaper? The answer lies in how insurers structure their drug lists-and not all combo drugs are treated the same.

How Insurance Tiers Work (And Why It Matters)

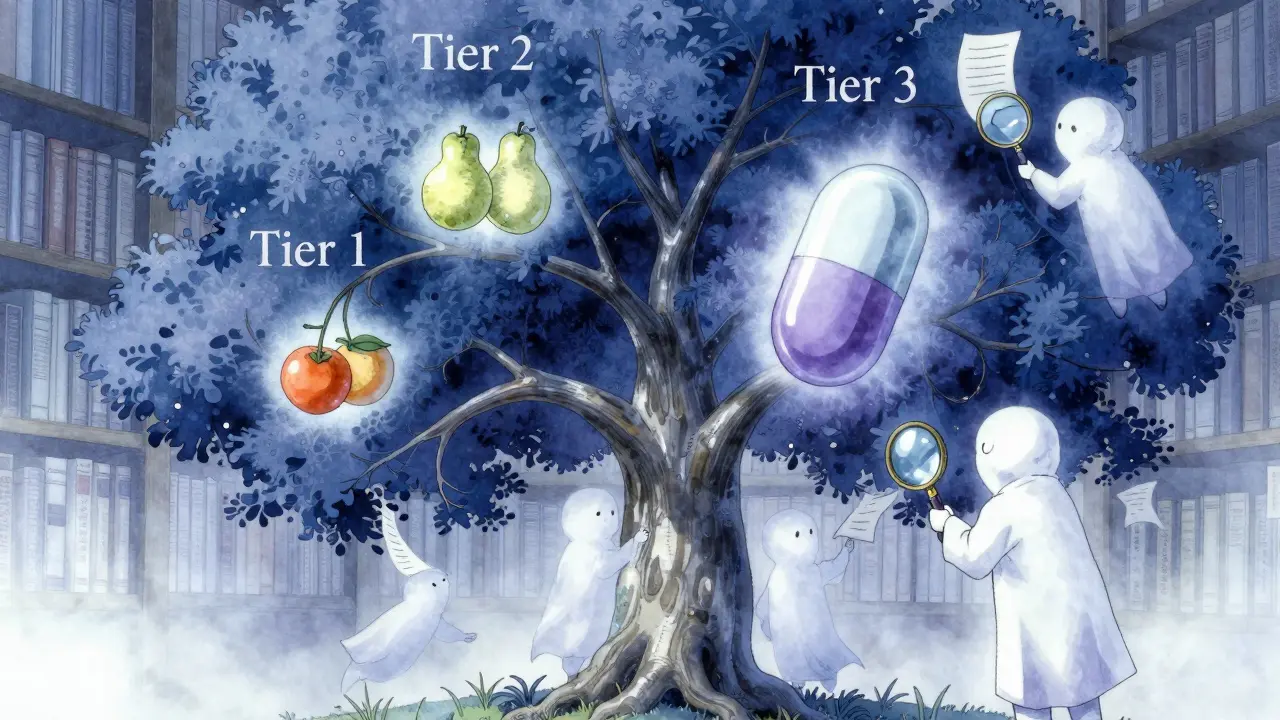

Most prescription drug plans, including Medicare Part D and private insurers, use a tiered system to control costs. Here’s how it typically breaks down:

- Tier 1: Preferred generics - copay as low as $0 to $5

- Tier 2: Non-preferred generics or preferred brand-name drugs - copay around $10 to $20

- Tier 3: Non-preferred brand-name drugs - copay $40 to $70

- Tier 4 (Specialty): High-cost drugs, often biologics or newer combos - copay $100+

Here’s the catch: not all combination drugs land in Tier 1. Even if both individual ingredients are in Tier 1, the combo might be placed in Tier 2 or 3. Why? Because insurers sometimes assume that taking two pills is just as easy as one-and they don’t want to pay more for convenience.

For example, a 2022 analysis of over 4 million Medicare Part D prescriptions found that 84% of plan-product combinations only covered generics. But within that group, coverage for combination drugs varied wildly. Some plans covered the combo in Tier 1. Others didn’t cover it at all unless you first tried the individual generics.

Why You Might Pay More for the Combo

It sounds backwards: one pill with two drugs costs more than two pills with the same two drugs. But it happens. Here’s why:

- Formulary placement: If the combo is on a higher tier, your copay jumps. Meanwhile, the two individual generics are still on Tier 1.

- Lack of competition: Some combo drugs are made by only one manufacturer (called "single-source generics"). Without competition, prices stay high-even if the ingredients are cheap.

- PBM incentives: Pharmacy benefit managers (PBMs) like CVS Caremark and OptumRx negotiate rebates with drugmakers. Sometimes, the rebate on individual generics is higher than on the combo, so the plan pushes you toward the separate pills.

A Reddit user in the r/Medicare community shared: "My plan covers the individual generics for $10 each but the combination product would be $50 even though it’s the same ingredients-I had to ask my doctor to write two separate prescriptions to save money."

That’s not rare. In fact, a 2023 Medicare Rights Center report found that 68% of beneficiaries needed help understanding their coverage decisions. Many didn’t realize they could ask their doctor to prescribe the two separate generics instead of the combo-just to save money.

When the Combo Actually Saves You Money

But here’s the flip side: sometimes, the combo is the cheaper option. When a combination drug goes generic and enters Tier 1, your out-of-pocket cost can drop dramatically.

One user reported: "When my blood pressure combo drug went generic, my out-of-pocket dropped from $45 to $7 per month with no change in effectiveness." That’s because the combo was now covered as a single Tier 1 drug-instead of paying $22 for each of two separate pills ($44 total), you pay $7 for one.

This usually happens when:

- The combo has multiple generic manufacturers competing

- The plan’s formulary committee decides the combo improves adherence

- There’s no rebate incentive to favor the individual pills

According to IQVIA, combination drugs make up only 15% of all prescriptions but represent 28% of top-selling drugs by volume. That’s because they’re often used for chronic conditions where taking multiple pills daily leads to missed doses. Insurers know this-and some now prefer combos for that reason alone.

How to Find Out What’s Covered

You can’t guess your coverage. You have to check. Here’s how:

- Use the Medicare Plan Finder: If you’re on Medicare, go to Medicare.gov and enter your drugs. It shows you exactly what tier each drug is on and what your copay will be.

- Call your pharmacy: Ask them to check your plan’s formulary for both the combo and the individual drugs. They can tell you which option costs less.

- Ask your doctor to write two prescriptions: If the combo is expensive, ask if you can get the two generics separately. Many doctors will do this without hesitation.

- Check for prior authorization: Some plans require you to try one or both individual generics before covering the combo. This is called "step therapy." If you’re denied, you can appeal.

Pro tip: In 2024, average generic copays ranged from $1 to $15. Brand-name drugs? $47 to $112. That’s why 90% of U.S. prescriptions are filled with generics. But not all generics are treated equally.

What Changed in 2024

The Inflation Reduction Act, which took effect January 1, 2024, made two big changes:

- No more Part D deductible: You no longer pay $505 out-of-pocket before coverage kicks in.

- $2,000 annual cap: Once you hit $2,000 in out-of-pocket spending, you pay $0 for the rest of the year.

These changes reduce the financial risk of choosing a more expensive combo-but they don’t change how your plan tiers drugs. So even with the cap, you might still pay more upfront if your combo is on a higher tier.

Another 2023 development: a federal court banned "copay accumulator" programs. These programs used to stop manufacturer coupons from counting toward your out-of-pocket maximum. That meant people on expensive brand-name drugs got stuck paying more. Now, those coupons count. That indirectly helps people on combos too-if you’re getting a coupon for a combo drug, it now counts toward your $2,000 cap.

What You Can Do Today

Don’t assume your insurance will pick the cheapest option for you. You have to be proactive.

- Compare the cost of the combo vs. individual generics at your pharmacy.

- If the combo is more expensive, ask your doctor to prescribe the two generics separately.

- Ask if your plan has a prior authorization or step therapy requirement for the combo.

- Use the Medicare Plan Finder or your insurer’s online formulary tool to compare tiers.

- If you’re denied coverage, file a coverage determination request-it takes 72 hours for a standard review, 24 for urgent cases.

And remember: just because a drug is "generic" doesn’t mean it’s automatically cheap. The real savings come from matching the right drug to the right tier-and knowing when to ask for something different.

Can I ask my doctor to prescribe two separate generic pills instead of a combo?

Yes. Many doctors will do this if it saves you money. The FDA confirms that individual generics are therapeutically equivalent to combination pills. As long as your doctor signs off and the doses match what the combo provides, your pharmacy will fill it. Just make sure the total daily dose of each ingredient adds up correctly.

Why does my insurance cover the combo but not the individual drugs?

That’s rare. Usually, if the combo is covered, the individual drugs are too. But sometimes, plans make mistakes or update formularies without clear communication. If you’re told the combo is covered but the individual drugs aren’t, ask for the formulary document and check the tier placement. You may need to file a coverage appeal.

Are generic combination drugs as safe as brand-name ones?

Yes. The FDA requires generic combination drugs to meet the same standards as brand-name versions: same active ingredients, same strength, same route of administration, and bioequivalence. The only difference is cost. Some patients report slight differences in side effects, but these are usually due to inactive ingredients, not the active drugs themselves.

What if my plan doesn’t cover the generic combo at all?

You have two options: ask your doctor to prescribe the individual generics separately, or file a coverage determination request. If your doctor states that the combo is medically necessary-for example, because you have trouble taking multiple pills daily-the plan must review your case. Expedited reviews are available for urgent situations.

Do all insurance plans treat generic combinations the same way?

No. Medicare Part D plans follow a general structure, but private insurers and employer plans vary widely. One plan might cover a combo in Tier 1, while another puts it in Tier 3. Pharmacy benefit managers (PBMs) like CVS Caremark and OptumRx set their own rules. Always check your specific plan’s formulary before assuming coverage.

Final Takeaway

There’s no one-size-fits-all answer. Sometimes the combo saves you money. Sometimes the two separate pills do. It depends on your plan, your drugs, and your pharmacy’s pricing. The key is to check before you fill your prescription. A quick call to your pharmacy or a quick search on Medicare.gov can save you hundreds. Don’t let confusion cost you-know your options, ask questions, and take control of your medication costs.