When you pick up a prescription, the price you pay at the pharmacy isn’t just the cost of the drug. It’s shaped by your insurance plan’s structure - and whether you’re getting a generic or a brand-name medication makes a huge difference. In 2024, the gap between what you pay for generics versus brand drugs wasn’t just noticeable - it was massive.

How Copays Work in 2024

Most prescription drug plans in the U.S. use a tiered system. Think of it like a pricing ladder. The lower the tier, the less you pay. In 2024, most Medicare and private insurance plans had four main tiers:- Tier 1: Preferred generics - cheapest option

- Tier 2: Non-preferred generics - slightly more expensive

- Tier 3: Preferred brand names - higher cost, but still covered

- Tier 4: Non-preferred brand names - most expensive

Some plans added a Tier 5 for specialty drugs - things like cancer treatments or rare disease meds. These often cost hundreds or even thousands of dollars per month.

Average 2024 Copay Numbers

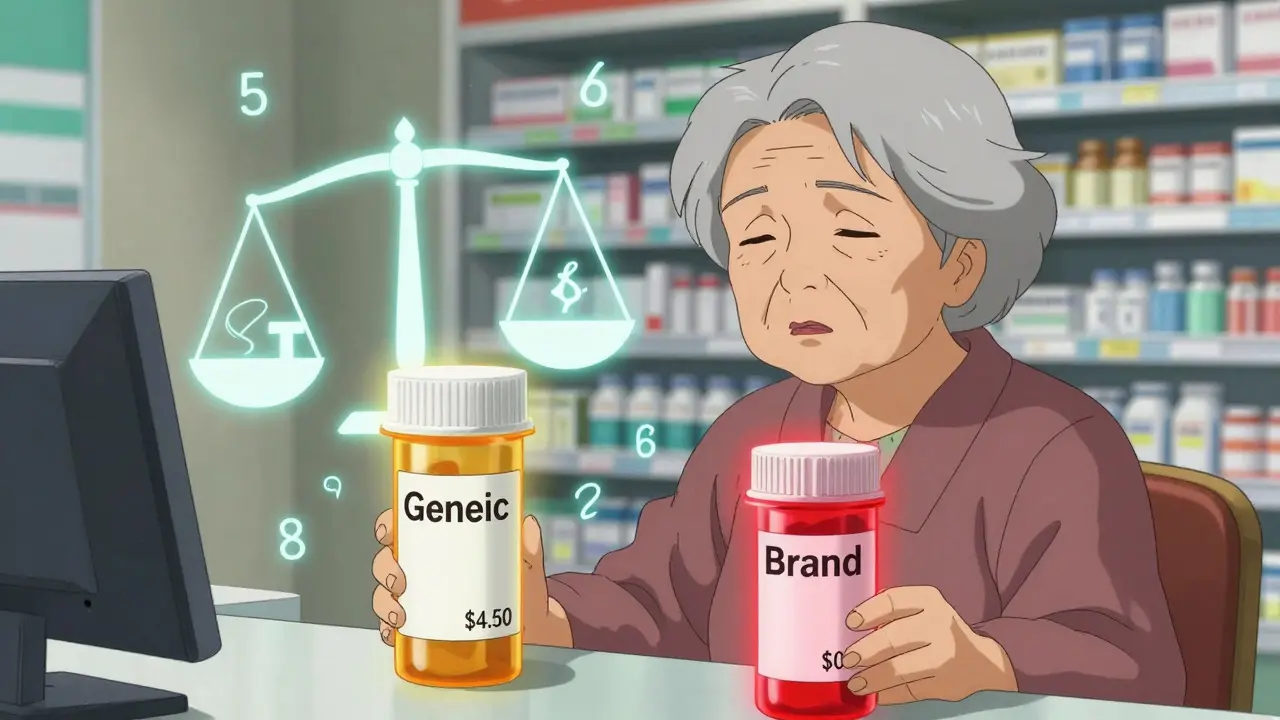

The numbers don’t lie. Here’s what most people paid out of pocket in 2024:- Generic drugs: $0 to $10 per prescription. For preferred generics, many plans charged just $4.50. Some even had $0 copays.

- Preferred brand drugs: Median copay of $47. This was the most common price for brand-name drugs that your plan encouraged.

- Non-preferred brand drugs: Median copay of $100. These were drugs your plan didn’t push - often because a cheaper generic existed.

For people on Medicare Advantage Prescription Drug (MA-PD) plans, these were fixed copays. You knew exactly what you’d pay. But if you were on a standalone Medicare Part D Prescription Drug Plan (PDP), you often paid a percentage - not a flat fee. That meant if your brand drug cost $200, you might pay 22% to 47% of that - so $44 to $94 - depending on your plan.

What About Commercial Insurance?

Private insurance followed similar patterns, but with more variation. Many plans used coinsurance instead of fixed copays. That means you paid a percentage of the drug’s total price. For generics, that might be 10% to 20%. For brand drugs? Often 30% to 50%.Some plans had a nasty trick: the "Member Pay the Difference" rule. If your doctor prescribed a brand-name drug - but a generic was available - you had to pay not just your copay, but the full price gap between the brand and the generic. One person in Texas paid $42 extra just because they chose Lipitor over atorvastatin, even though their doctor said "dispense as written."

Extra Help? Lower Costs

If your income is low, you might qualify for Medicare’s Extra Help program. In 2024, that meant:- Maximum $4.50 copay for generics

- Maximum $11.20 copay for brand drugs

That’s a big deal. Without Extra Help, someone taking a $100 brand drug could pay the full amount. With it, they paid $11.20 - no matter what.

Why the Huge Price Gap?

Generic drugs are chemically identical to brand names. They’re just cheaper because they don’t need to pay for research, marketing, or patents. In 2023, generics made up 92.7% of all prescriptions - but only 17% of total drug spending. That’s because brand drugs cost so much more.Medicare Part D spent $1,027 per person on generics in 2023. On brand drugs? $7,842 per person. That’s almost eight times more.

But here’s the twist: even though generics are cheaper to make, their prices in the Medicare system aren’t always low. Some pharmacies and wholesalers inflate generic prices to keep favorable deals on brand drugs. Independent pharmacists have reported being forced to pay more for generics just to get access to branded drugs - which then affects what you pay at the counter.

What’s Changing in 2025?

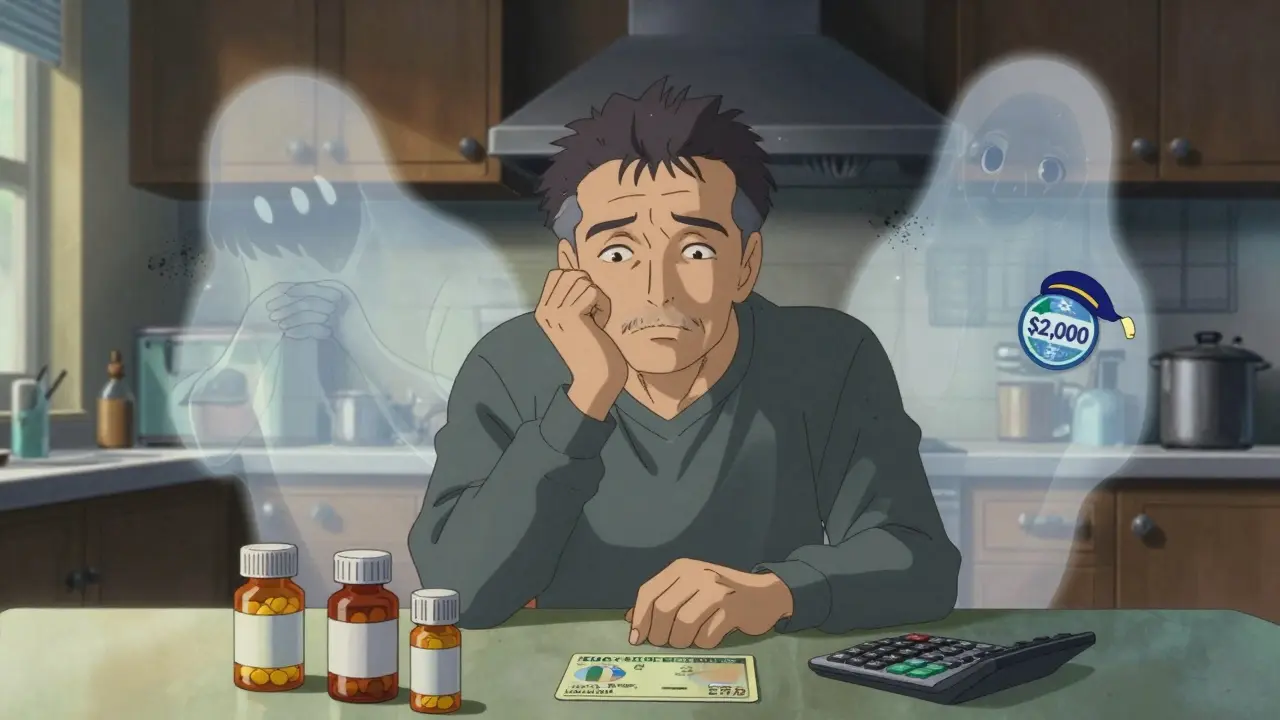

The Inflation Reduction Act didn’t just tweak things - it overhauled them. Starting in 2025:- The annual out-of-pocket maximum for all drugs drops to $2,000. No more $8,000+ spikes.

- 98% of Medicare Part D plans will have $0 copays for preferred generics - up from 87% in 2024.

- Insulin costs are capped at $35 per month - no matter if it’s generic or brand.

These changes mean people on expensive brand drugs will save the most. But even those on generics will benefit. The $2,000 cap will stop surprise bills when someone needs multiple medications.

Real Stories, Real Costs

One retiree in Florida told a Medicare forum: "I pay $95 a month for my brand-name drug. The generic would cost $15. My doctor won’t switch me because of side effects. I’m stuck." A 2024 survey of 1,200 Medicare beneficiaries found:- 63% of people taking brand drugs struggled to afford them

- Only 28% of people taking generics had the same problem

Complaints about unexpected brand drug costs made up 37% of all prescription drug complaints in Q1 2024 - more than triple the number for generic-related issues.

How to Save Money Right Now

You can’t change your plan mid-year - but you can still take control:- Check your plan’s formulary. Every plan must publish it by October 15. Use the Medicare Plan Finder to enter your exact drugs and see real costs.

- Ask your doctor about alternatives. 72% of Medicare plans have a generic version for at least 80% of common brand drugs. Maybe your drug has a cheaper cousin.

- Calculate annual cost, not monthly. A plan with a $5 generic copay and $100 brand copay might cost you $1,200 a year if you take one brand drug. A plan with $0 generics and $40 brand copays? Just $480.

- Consider Extra Help. If your income is under $22,000 (individual) or $29,000 (couple), you likely qualify. Apply through Social Security.

- Use cash prices. Sometimes, paying cash at Walmart, Costco, or CVS is cheaper than using insurance. Check GoodRx or SingleCare before you pay.

Final Takeaway

In 2024, the difference between generic and brand drug costs wasn’t just about savings - it was about survival. For many, choosing the generic meant eating, paying rent, or keeping the lights on. For others, the brand was non-negotiable - and they paid the price.The system is shifting. By 2025, the $2,000 cap will protect everyone - but until then, knowing your plan’s tiers, checking your drugs, and asking questions can save hundreds - or thousands - a year.